JACKSONVILLE, Fla. – Hurricane Preparedness Week (May 5-11) is your time to prepare for the potential of a tropical storm or hurricane.

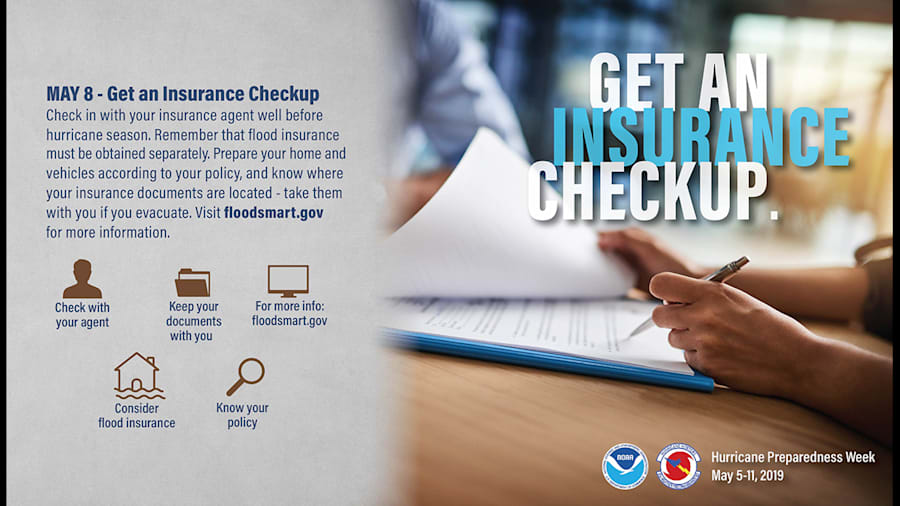

Tuesday's focus is home insurance and you are urged to seek out a homeowner's insurance check up.

Recommended Videos

Call your insurance company or agent and ask for an insurance check-up to make sure you have enough homeowners insurance to repair or even replace your home. Don’t forget to ask about coverage for your car or boat.

Have your agent print out your policy for you and explain the different elements, especially relating to storm coverage. Often times you have a separate deductible for damage incurred during a hurricane or tropical storm and it can be much higher that your traditional deductible.

Remember, standard homeowners insurance doesn't cover flooding. Whether you’re a homeowner or renter, you’ll need a separate policy for it, and it’s available through your company, agent or the National Flood Insurance Program by clicking here. It is important not to wait until closer to hurricane season, as flood insurance requires a 30-day waiting period.

According to the National Flood Insurance Program (NFIP), floods cause billions of dollars in

property damage in the U.S. every year. If you live in a high-risk area, your home has a 26% chance

of being damaged by flooding during the course of your 30-year mortgage, compared to a 10% chance

of being damaged by house fire.

Also ask your insurance agent about the process after the storm if you have damage to your property. He or she can walk you through the process, explaining how adjusters will survey the damage and make an estimate of the cost of repair. Ask if you can use any licensed contractor or if you are bound to use the insurance companies' assigned contractor.

Basic questions to ask your insurance agent from FLASH

- What coverages are appropriate for my living arrangement?

- Who sells these coverages?

- What coverages do I need to purchase? Are they available?

- What perils are covered in the policy I purchase?

- What is the proper amount of insurance to purchase?

- Are there steps I can take to lower my premium?

Types of insurance policies – What’s right for you?

Several lines of insurance are available to cover various perils. The most appropriate

insurance product for your needs depends primarily on your type of dwelling.

Owning a Home – If you own a home, there are two available policy forms: homeowners

and dwelling forms. The main difference between these two types of forms is that the

homeowners form combines property coverage with liability coverage, while the dwelling

form only covers property losses. In addition, a dwelling form is more typically used for a

dwelling that an insured person owns but does not live in, or only lives in during part of the

year. Both types of policy forms have the various peril coverage available for both the dwelling

and its contents.

Owning a Manufactured Home – There are policy forms specifically designed to insure

manufactured homes. This type of policy covers both the dwelling and contents and provides

liability protection.

Owning a Condominium – There are policy forms specifically designed to cover

condominiums, which typically cover contents (i.e. your personal property) and liability.

A small amount of dwelling coverage is provided to cover the portions that you are

responsible for, as defined by the governing rules of the condominium association.

This may include condominium common areas, and you can purchase additional

dwelling coverage if the protection included in the package is insufficient.

Renting a Residence – There are renter’s insurance policy forms specifically designed for

you if you are renting and do not own your residence. These forms provide coverage for your

contents and liability.

Owning a Home on a Farm – Farm owner’s policy forms are specifically designed to

cover farms or ranches which may not qualify for standard homeowners insurance. This

policy may be the most appropriate form to cover property losses to your home, and other

structures such as barns and silos, from the damage of tornadoes, hail, and other perils.

Farm owner’s policies also cover both the personal and commercial exposure of farms, along

with liability coverage.

For more detailed information about homeowners insurance policies and what they cover during times of disaster, click here to download FLASH's guide to insurance